As a small business owner, you’ve probably heard of Small Business Association (SBA) loans. These loans are geared towards supporting small businesses across the US. Issuing banks face a lesser lending risk with SBA loans. This is because these loans guarantee a portion of your borrowings. An SBA loan can be applied for through credit unions, local banks or any approved financial lenders.

There are numerous types of SBA loans, and they can range anywhere from thousands to millions. They can be used for various small business financing needs which might include:

Pros

SBA loans can be a great solution for businesses who don’t qualify for a traditional bank loan. They’re also more affordable because of their interest rate caps. Fixed asset loans are collateralized by the asset, so there’s no need to commit personal assets. Additionally, the SBA offers a lot of free education and business information to small business owners.

Like bank loans, obtaining loan approval can be hard and takes a long time—usually at least two months. In order to get a larger loan, you’ll need collateral (usually personal assets) and a downpayment, so you need very high confidence that you can pay it back. If you have poor credit or limited financial history, it’s unlikely you’ll be approved.

Bottom Line

A small business loan is a good option if you didn’t qualify for a traditional bank loan or want better terms, and if you have a solid business history and the time to invest in the process.

Business credit cards can be issued by your bank or a credit card company. Business credit cards are different from personal credit cards, typically allowing for larger spending limits and providing more perks. They can be secured or unsecured.

Pros

There are numerous options for small business credit cards, and you can get more than one. Most business cards offer quick, easy, and convenient access to funding as well as rewards, cashback schemes, and interest-free terms of up to 90 days. As you pay off the balance, you can build your credit record, which can help you get more significant financing later. You or your employees can use credit cards for ordering supplies and paying business expenses quickly while tracking them and keeping them separate from personal spending.

Small business credit cards can tempt business owners to overspend. They can be liabilities if lost, stolen, or abused by employees, so it is important to have controls and limits in place. Credit cards are not scalable for larger financing needs because of their very high interest rates and spending limits. Additionally, you may experience a negative impact on your credit score if you make late payments or maintain large balances over a long period of time.

Responsible use of small business credit cards can enhance your credit score, keep track of expenses, and improve cash flow while receiving perks, but they are not a scalable long-term financing solution.

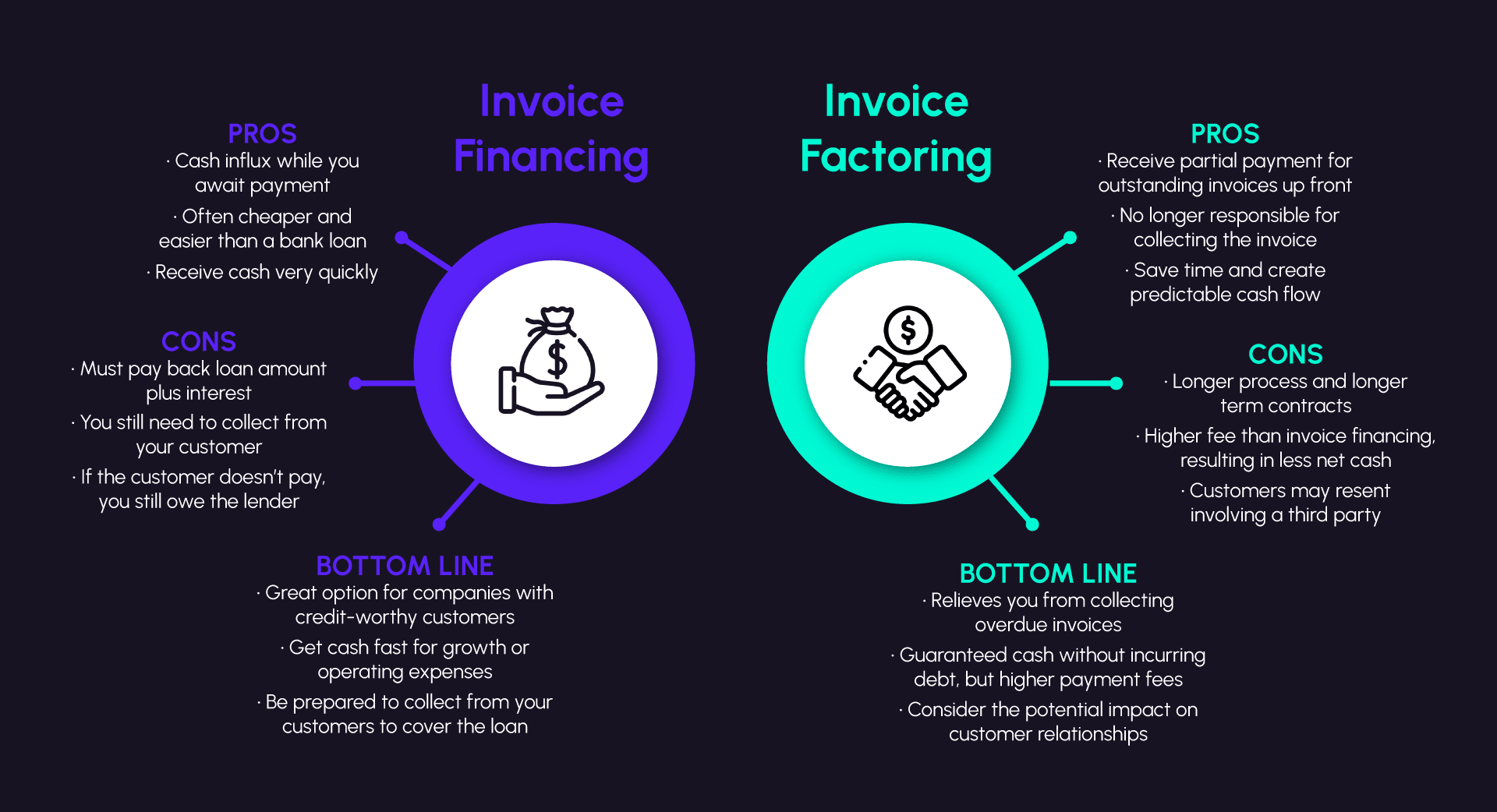

Invoice factoring and invoice financing are similar concepts. In this case, however, you are selling some or all of your company’s unpaid invoices at a discount, typically 10%-20% of the invoice value. Your invoices are then owned by the factoring company, and they are responsible for collecting payments directly from your customers. You will receive the remaining invoice amount, minus a fee, once your customer has paid the full amount.

Pros

In addition to the pros listed for invoice financing, particularly if you have longer term outstandings, using invoice factoring will allow you to have more predictable cash flows and reduce your risk. The elimination of debt collection responsibilities can also save your company a lot of time and money.

It takes time to arrange factoring while waiting for the third party to validate invoices. Factoring is not suitable for companies with a few customers only because factoring companies want to spread their customer risk as widely as possible. These companies may also require long contracts of two years or more because of the risks involved. They also charge a higher fee than invoice financing due to the added risk of collecting from your customers. Factoring companies may also be perceived by customers as a sign that your business isn’t doing well, and your customers may resent having to deal with a third party.

Bottom Line

Factoring can help your company when it has a lot of longer term outstanding invoices, you don’t have time or resources to chase down payments, and as a result your cash flow is suffering. Be careful to weigh these benefits with the impact on your customer relationships.

Small businesses can raise money online through crowdfunding by offering equity, rewards, or debt to investors. Many people think of crowdfunding as an option for startups, but established small businesses can raise funds online as well, especially if they manufacture or sell products, have a high growth business that can be easily expanded, or have an innovative technological solution.

Examples of crowdfunding platforms include Kickstarter, Indiegogo, Fundable, and SeedInvest.

Examples of crowdfunding platforms include Kickstarter, Indiegogo, Fundable, and SeedInvest.

Pros

Crowdfunding platforms offer low fees, a large audience of potential investors and customers, and allow for a variety of funding campaigns.

Crowdfunding loans for small businesses require a strong promotional strategy, transparency, and possibly giving up some equity in your business. There are many projects and businesses competing on each crowdfunding platform so it can be hard to get noticed. Some platforms can have high fees.

Crowdfunding can be a great option if your small business needs to increase sales quickly, or if you need funding for product line expansion. You have to be organized to promote your business and possibly willing to give up equity.